Dear Valued Clients:

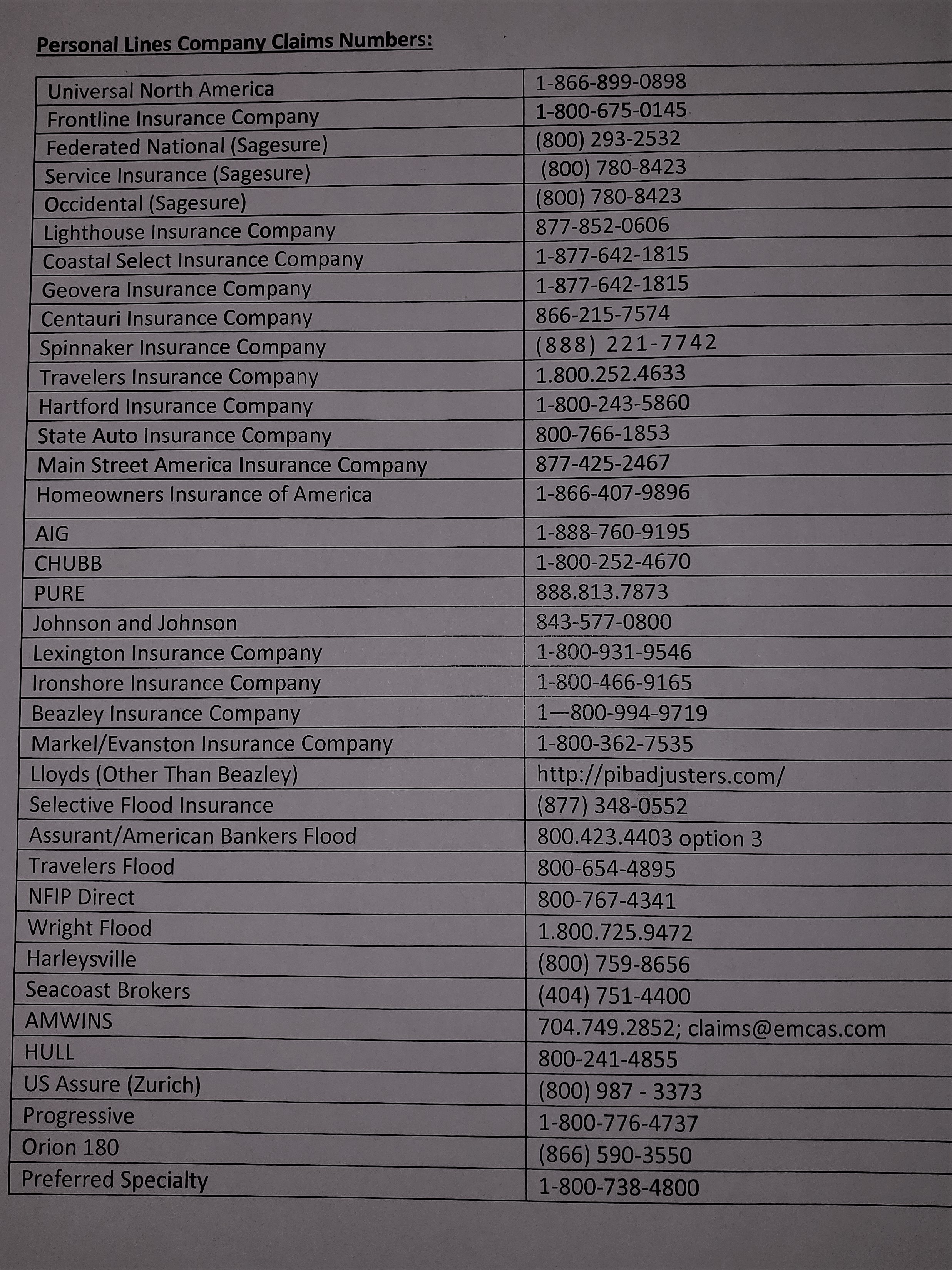

In the event of a major hurricane and mandatory evacuation, our agents will also be seeking shelter from the storm with their families and loved ones. Below is a list of the direct phone numbers for our most popular personal lines insurance carriers. The carrier’s claim number can also be found on your declarations page. Please call as soon as you suspect damage to get in the wait line for an adjustor to call you as there will be a significant claim volume. Upon our return to the office, we will be able to file these claims for you.

Please stay safe and know that we will be back as soon as reasonably safe to help our clients through this catastrophe.

The Aftermath

In the event of damage to your property, please click the link below that outlines the steps to take. Please also check our previous post for a easy to navigate list of our personal lines carriers and their claims numbers. We are happy to take your claims when we return to the office, but with the abundance of claims that will be reported we recommend to get your claim called in to get in line for an adjustor. A list of company claims number can be found here and on our Facebook page for client reference. The claims will be handled in the order the claims come in

.

Above all, stay safe! Your “stuff” can be repaired or replaced. You cannot!

Sincerely,

Your Agents at McKay Insurance, INC